Hedge fund Renaissance Technologies is looked upon by Wall Street with awe and envy in equal measure. Particularly, Medallion Fund, an employees only fund it runs. Bloomberg last year wrote the fund has returned more than $55 billion, making it more profitable than funds run by feted veterans such as George Soros.

The Renaissance flagship fund, which will turn 30 next year, has returned more than 25% profits in most of its years of investing. Money doubles in a little more than three years at that rate. Medallion turned in 40% or thereabouts in 13 of its years; at that clip, money almost doubles in just two years.

In this satellite city of capital New Delhi, a computer scientist and a finance whiz with roots in computer science are on the Renaissance track. They have primed and started up AccuraCap, a fund management firm that runs on a mathematical model straddling big data analytics and artificial intelligence

Medallion is not just another league table topper. The investment strategy and operations at New York-based Renaissance is run by complex mathematical models written by math Ph.Ds and baked into code by the best of computer science brains. Code that takes its cues from market movement and picks and dumps stocks, bonds and other financial instruments at lightning speed, with almost no human intervention. Purists among quants, as the math and computer scientists behind such market software are called, will baulk at the “almost” in the previous sentence. Humans mess with their models, they insist, and shouldn’t have any decision-making role in trades.

New York and Noida have little in common except the 14th letter of the English alphabet their names start with. But, in this satellite city of capital New Delhi, a computer scientist and a finance whiz with roots in computer science are on the Renaissance track. They have primed and started up AccuraCap, a fund management firm that runs on a mathematical model straddling big data analytics and artificial intelligence. Accuracap has a team of just seven people, including its founders Naresh Gupta (third from left) and Raman Nagpal (fourth from left) working with its proprietary model

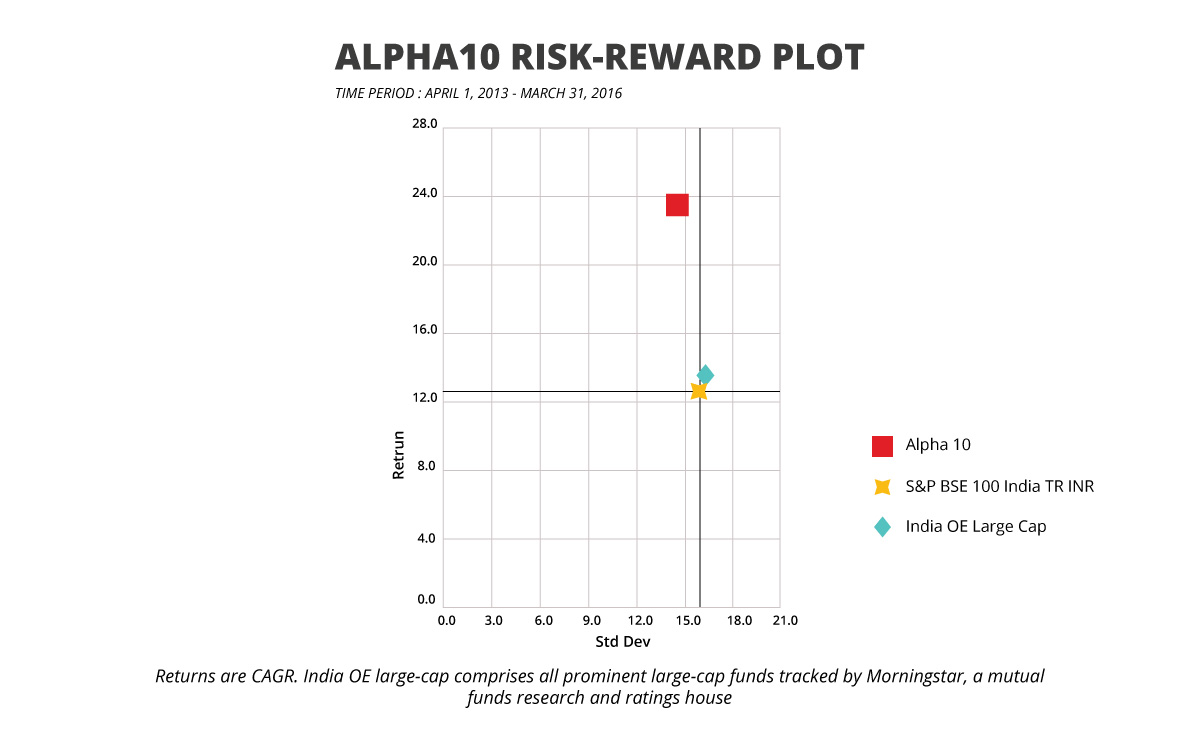

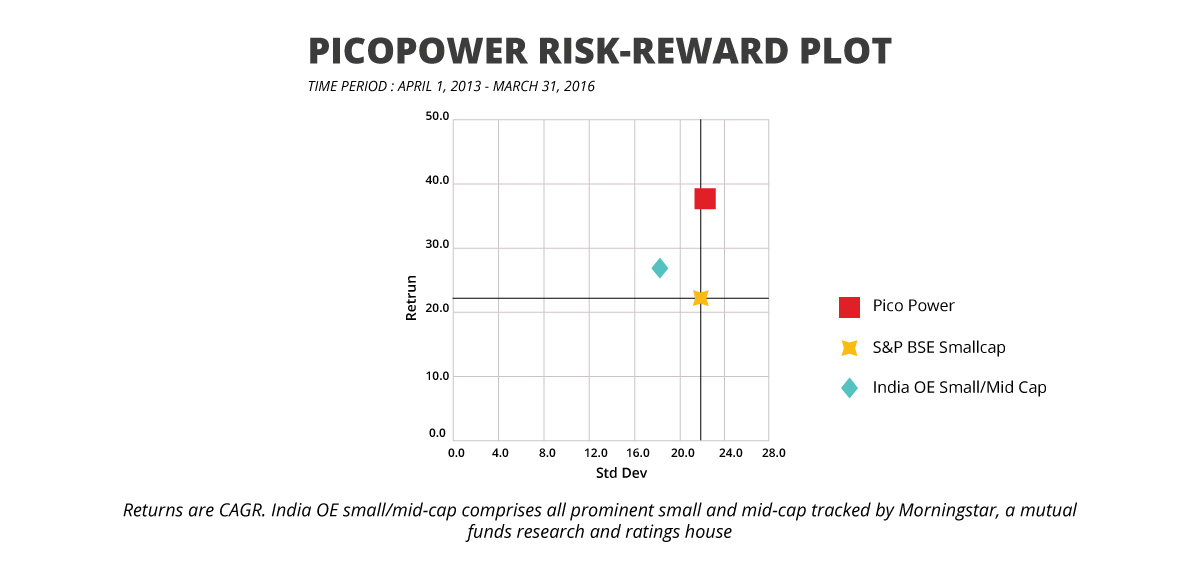

The fund house has a modest Rs 800 crore size — and maket-beating, off-charts returns. A small cap fund it runs, called Pico Power, has returned 185% in four years to January 31, 2017 at a time the comparable BSE Smallcap index grew 77%. Alpha 10, AccuraCap’s big cap fund, reeled in a 101% versus the BSE 100’s 45% expansion. (The risk-reward graphs published later in this story show the risk of the two funds are lower than or comparable to that of their segment indices.)

For comparison’s sake, Pico Power is the best performing among its peers, according to AccuraCap data up to January this year, outgunning the likes of DSP BlackRock Micro-Cap Fund, Franklin India Smaller Companies Fund, and Canara Robeco Emerging Equity Fund. Alpha 10, too, is grouped at the top neck and neck with Reliance Top 200 Fund and Birla Sun Life Top 100 Fund.

All this has been achieved with a team of just seven people, including founders, in AccuraCap— working with its proprietary model.

The fund house has a modest Rs 800 crore size — and maket-beating, off-charts returns. A small cap fund it runs, called Pico Power, has returned 185% in four years to January 31, 2017 at a time the comparable BSE Smallcap index grew 77%. Alpha 10, AccuraCap’s big cap fund, reeled in a 101% versus the BSE 100’s 45% expansion

Naresh Gupta and Raman Nagpal, the men behind AccuraCap, call themselves “inventors” at the firm. Both were top managers at the India subsidiary of digital media software maker Adobe Inc. — Gupta until March 2015 and Nagpal until July 2015. They make for the perfect partners in a fund built on big data analytics and AI. Gupta is the quintessential geek and tech manager with a deep interest in AI. His Ph.D was in image processing and pattern recognition, an area steeped in fuzzy logic. Early in his career he was the director of the AI group at LNK Corp, a US department of defense backed company). Nagpal, who brings investing and markets smarts to the table, holds a CFA and MBA after graduate and postgraduate degrees in computer science.

Like most busy, fast-track professionals, Gupta and Nagpal never found time to directly invest in stocks and routed their money in the markets via mutual funds. By 2006-07, Gupta says, it was clear that he could sweat his investments better than mutual funds. Nagpal and he were thick friends by then and used to exchange thoughts on how to go about it in a scientific way.

The market-beating box

The investment philosophy of US value investor and professor at Columbia Graduate School of Business, Joel Greenblatt, made sense to the left-brained duo. His book, The Little Book that Beats the Market, first published in 2005, detailed his investment strategy at the Gotham Fund he ran and reported market-beating returns. The Gotham premise was simple: if you invest in stocks with a combination of high RoCE (short for return on capital employed, a measure of capital efficiency) and a reasonable valuation — measured by enterprise or total value divided by earnings before interest and tax — and are disciplined about it, you can do much better than the market.

“We said this is a simple thing. Let’s try this in India. We implemented the idea in 2007. It didn’t initially work well but it got us started,” says Gupta, who had led the December 2005 $3.5 billion acquisition of Macromedia for Adobe. “We asked ourselves why the model of Greenblatt didn’t work so well in India.”

The missing link was that India is a strong growth market. “Unless you factor in that growth, you don’t end up beating the market because it is moving very fast,” says Gupta, in an interview in a sparse conference room in the AccuraCap office. It is on the ninth floor of an office tower that stands in a crowded Noida market bustling with sweets shops and garment sellers doing brisk business, cigarette and paan sellers making a living in four-by-four feet stalls, hole-in-the-wall automobile repair shops fixing motorbikes, and cycle rickshaws jockeying for space with honking cars — all signs of the fast growing economy and a matching swinging stock market that India is home to.

Nagpal and Gupta were already strong believers that fundamentals of a company drive its stock performance but they couldn’t reconcile to the logic of predicting future business performance. “The past is all facts, the future is all up there,” Gupta says with an upward wave of his hands. “Usually, all the Excel sheet analysis you do has a low likelihood of coming true.” The conclusion was: if you look at the past performance of companies very closely and create a good portfolio based on that, you are going to be better off than trying to look into the future on what or how companies will do.

The conclusion was: if you look at the past performance of companies very closely and create a good portfolio based on that, you are going to be better off than trying to look into the future on what or how companies will do

“Starting from there, we created our model which looks at millions and millions of data points both in terms of the business fundamentals of all the companies that are in the landscape over the last five-seven years and, the stock price of all the stocks in the last five-seven years. And, based on that, it comes up with a set of rankings,” says Gupta. The ranking set normalises performance of companies from different industries making comparisons and calls across the market easier.

Some of the data sheets in the AccuraCap model have gigabytes of data, not surprisingly.

The model does not run on AI platforms such as IBM’s Watson. It has been written ground up by Gupta and Nagpal, spending over a combined 15,000 hours at it, according to an AccuraCap presentation. Before the interview with FactorDaily, Gupta had made it clear he wouldn’t show how the model works. At the meeting, too, he is thrifty with details; he says AccuraCap doesn’t want to patent the model because that will mean details, however, sketchy, will have to be made public.

Still, he agrees to give the broad contours of the black box at AccuraCap. “We have encoded our business understanding and logic into the model,” he says. There are three check boxes at the core of the fund’s black box: A stock should be available inexpensive (“I don’t want it cheap, I just want it relatively inexpensive.”). The company should have demonstrated consistent, market-beating business difference that it is able to grow business and profits (“Something must be working right for it.”). It shouldn’t have too much risk (“Has the promoter done shady things in the past, is the company leveraged, what are the industry risks…?”).

“Starting from there, we created our model which looks at millions and millions of data points both in terms of the business fundamentals of all the companies that are in the landscape over the last five-seven years and, the stock price of all the stocks in the last five-seven years. And, based on that, it comes up with a set of rankings” — Naresh Gupta

Add to this the discipline of staying put and the resisting the urge to churn the portfolio. Though the entire equity landscape is tracked real time and rankings in the subsets that Pico Power and Alpha 10 invest can change at any time, AccuraCap allocates and reviews portfolios once a year with quarterly rebalancing. This works best, insists Gupta, admitting to having egg of his and his team’s face when they tried to intervene. (This is exactly the lesson that the run on US markets following mortgage defaults in the autumn of 2007 taught Renaissance traders: don’t mess with the model.)

“This [model] is our understanding of the investing business and over time I have figured out several other factors and how it should adjust to different kinds of market situations,” summarises Gupta. “What neural networks can do is find patterns that none of us ever see. Some of these fuzzy logics have actually found some patterns.” It is clear he won’t say more no matter how you try to tease information out.

Will AI have Dalal Street for lunch?

Over its eight years of being, AccuraCap has built confidence and plans to bulk up. Gupta says a few foreign investors — he doesn’t identify them — are interested in putting the big bucks behind AccuraCap. He doesn’t say how much he expects the fund’s Rs 800 crore size to grow, limiting himself to “it could be anything… a multiple…”.

There are sceptics in the market, meanwhile. Seasoned fund manager Nilesh Shah makes the point that technology does indeed give arbitrage trading like a shot of steroids, evidenced in how so-called algorithmic trading — trades executed per some preset conditions — has topped 40% of total trades in India. (Such high speed, automated trades are more than 80% in markets such as the US.)

But, “in fund management, naked eyes have an advantage,” says Shah, managing director, Kotak Mahindra Asset Management Co Ltd. “If you look at the HFCL balance sheet, you will never able to figure out the governance there. If you look at Deccan Chronicle, you will not know how badly leveraged they are,” he says giving examples of corporate and accounting transgressions that a machine may find hard to spot. “It is gut feel that plays out in such situations and (AI, big data analytics) will have to develop the competence to match naked eyes. It could take six months or a few years.”

“It is gut feel that plays out in such situations and (AI, big data analytics) will have to develop the competence to match naked eyes. It could take six months or a few years” — Nilesh Shah, managing director, Kotak Mahindra Asset Management

Scale could be the other limiting factor, Shah adds, without referring to AccuraCap. “What works on a Rs 100 crore machine strategy may not work on a Rs 1,000 crore machine strategy or on a Rs 10,000 crore machine strategy. The Tendulkar at 16 was very different from the Tendulkar at 24 from the Tendulkar at 30 and the Tendulkar at 35,” he says referring to limitations of any AI-led model as it moves to larger fund sizes and different market conditions.

Nagpal is stoutly confident of what can be built from here and scoffs at the suggestion of an exit. “We have not been bought not because there hasn’t been interest but because we are not up for sale,” he says when I meet him briefly at the end of the Gupta interview. About half of the Rs 800 crore funds that AccuraCap manages is from Gupta, Nagpal and their close families; the rest from about 400 investors.

AccuraCap has so far been structured as a portfolio management scheme (PMS) that allows participating investors to invest directly from their demat accounts. It charges them 1.5% of the fund size (technically, called assets under management or AUM) as a fixed fee. (Stock markets regulator Securities and Exchange Board of India caps commission at 2.5% of AUM for equity funds.)

In a not-so-common commission structure in India, AccuraCap takes a one-fifth cut of something marketmen call “alpha”. Alpha is the excess return of a fund or portfolio relative to the market. For example, if the market goes up by 10% and your portfolio rises 10%, alpha is zero. But, if the market moves up 10% and your portfolio expands 20%, alpha is 10%. In such a situation, AccuraCap will charge an investor 20% of 10% — 2% as commission. Most PMSs charge commission on absolute returns making them more expensive.

The opportunity “is to build something large” springboarding from the learnings so far, adds Gupta. This will necessarily involve engaging with overseas investors who have deep pockets — typically, family offices of wealthy individuals, university endowment funds, pension or other funds looking for an exposure to the Indian market as part of diversifying their investments.

In the years ahead, AccuraCap’s success will depend on how it layers machine learning and deep learning techniques as part of getting AI and big data analytics to juice more out of its model

Even when that happens and AccuraCap’s fund size expands several times, Gupta sees AccuraCap’s staff expanding by only a few people: “Perhaps to handle operations, compliance etc. not for core investing because that is done by the model.”

He also believes the AccuraCap black box can be replicated across equity markets — or spread to other instruments — in other countries, as well. The model can, for instance, operate in the cash market as also the futures and options segment. “For some of our global customers, we do plan to use the F&O segment,” he says. AccuraCap has so far not invested in F&O markets making its returns even more impressive because often funds play in the segment to boost performance despite higher risk.

In the years ahead, AccuraCap’s success will depend on how it layers machine learning and deep learning techniques as part of getting AI and big data analytics to juice more out of its model. (Read a primer on machine learning and deep learning here.) Its experience of the past few years has been instructive and showcases the potential of not just generating consistent high returns but also disintermediating specialists in the funds management business.

How fast that trend will accelerate is not clear but there are some in the mainstream fund management business who sound a note of caution.If IBM Watson can beat the Jeopardy champion or Google DeepMind can best a Go grandmaster, says Navneet Munot, Executive Director and Chief Investment Officer, SBI Funds Management Private Ltd, “asset managers like us should be paranoid about what technology can do to our business.” Indeed, yes.

FactorDaily’s journalism is produced by some of the best brains in the story-telling business. If you like our body of work – deep reportage, domain specialist write-ups, data stories, podcasts and the like – consider supporting the FactorDaily journey.